Normal Balance of Accounts: Definition and Examples

Learn about normal balance in accounting, including debits and credits, T-accounts, and practical examples to improve your financial record-keeping.

.png)

.avif)

In financial accounting, a normal balance refers to the debit or credit balance that’s normally expected from a certain ledger account. This concept is commonly used in the double-entry method of accounting.

In a business asset account, for instance, the normal balance would consist of debits (i.e., money coming in). You expect your asset account to have a debit normal balance. Conversely, in a business liability account, the normal balance would consist of credits (i.e., money you owe). You expect your credit account to have a credit normal balance.

Understanding the normal balance of an account and its position in double-entry accounting can help support good accounting practices in your business.

What is a normal account balance?

To understand normal balances, it’s important to understand the T-account model. A T-account provides a visual overview of a single account using a “T” shape, with debits (additions to the account, or positives) on one side of the account, and credits (subtractions to the count, or negatives) on the other side of the T.

Here’s an example of a standard T-account for a business showing debits on the left side (the debit side) and credits on the right side (the credit side). This example is for a business cash account, which is a type of asset account.

In this case, the debits on the left-hand side would be considered the normal balance of the account because it’s a cash account, which is considered an asset account. The debits on the left-hand side reflect this positive value.

Understanding debits and credits

A better understanding of debits and credits can help clarify the normal balance concept. “Debit” and “credit” are terms used in a double-entry accounting system.

In this system, each business transaction is recorded twice, in two distinct accounting book journal entries: one for debit and another for credit.

In addition to tracking revenue and expenses accounts, the double-entry accounting method tracks assets, liabilities, and equity accounts by recording transactions in at least two accounts. This contrasts with the single-entry method, which typically tracks only expense and revenue accounts and doesn’t provide a complete picture of a business’s financial position.

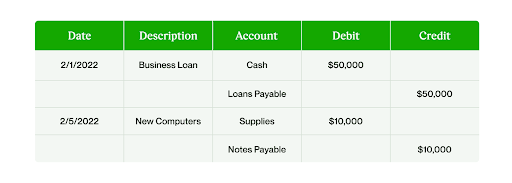

Let’s say you take out a business loan of $50,000. Technically, this means you have +$50,000 going into your cash account. However, this money is a loan, so it also creates a liability (that is, you would also note the $50,000 in your liability account).

In the same month, you purchase $10,000 worth of new computers. Technically, you’ve increased your business’s assets by $10,000 and you’d note this in your business’s asset account. However, you purchased the computers on credit—so, you’d also note the cost of computers in your notes payable account.

Here’s how that might look in your double-entry accounting system:

Each transaction has two corresponding journal entries. At a glance, you can see which accounts are affected and how. Since the debits and credits for each entry come to zero, this would be considered a balanced general ledger.

How does the normal accounts concept factor in here? The cash account is an asset account and has a normal debit balance. The loan payable account is a liability account and has a normal credit balance. The supplies account is an asset account and has a normal debit balance. The notes payable account is a liability account and has a normal credit balance.

The equation

Normal balance relates to the basic accounting equation that forms the basis of double-entry bookkeeping:

Assets = liabilities + owner’s equity

This equation tells you if an account is affected by a debit entry or a credit entry. The normal balance refers to the debit or credit balance expected.

If you need help with your calculations, Upwork can connect you to independent bookkeepers who have the expert knowledge you need.

How a normal balance works

Normal balances

Seeing an example of how a normal balance is found can help provide clarity. Let’s take the example from above.

This is the overview you’d see in your double-entry accounting system. However, note the different types of accounts referred to:

- Cash

- Loans payable

- Supplies

- Notes payable

Look below to see how each account might be represented. This shows how the debit or credit entry affects the account and presents the normal balance.

Let’s start with the cash and supplies accounts. Cash and supplies are both asset accounts. In these instances, the normal balance is a debit balance.

Next are the loans payable and notes payable accounts. Loans payable and notes payable are both liabilities accounts. In these instances, the normal balance is a credit balance.

Accounts chart

When you compile the above data into an accounts chart you can see whether all of your accounts have the expected normal balance. This quick chart tells you what the normal balance is for each type of account. You can also see how a debit or credit entry impacts each type of account.

Here’s what a chart of accounts might look like:

A practical normal balance example

A final normal balance example can sum up the information above. Let’s take a business asset account, which should have a normal debit balance. You want to make sure this is the case for this specific business asset account. Take a look at the business cash account for March.

The asset account’s normal balance should be on the debit side. This is the case here, as the balance has a debit of $3,000 on the left-hand side.

Now, let’s say the business cash account wasn’t what you expected. Instead of having $3,000 on the debit side, it shows $3,000 on the credit side—this isn’t what you want for an asset account.

In this case, you’d want to figure out why the account isn’t showing a normal balance. You might have had a journal entry error, an offset from an earlier transaction, or even checks written but not yet funded with cash.

Keep track of your financials the right way

Accurate accounting ensures your small business stays on top of its financial obligations. Doing this right is also a way to measure your business’s success over time, providing valuable insights that can inform your long-term financial planning.

The information in your accounts will also be used to compile financial statements, such as balance sheets and income statements, for shareholders and other external parties.

You may choose to manage day-to-day financial records using finance apps and other tools. These can help you track various aspects of your business, from service revenue to depreciation of assets. Some systems even allow for accrual accounting, which can provide a more accurate picture of your financial health over time.

However, when you need to deal with complicated accounting equations and generating financial statements, the job is best left to a professional. They can help you navigate complex issues like handling common stock or managing a contra asset account.

Look for qualified independent bookkeepers on Upwork, which provides a global pool of talented professionals to choose from. You can browse independent professionals according to price and reviews, so you get the right expert for your business’s needs.

.avif)

Author Spotlight

Upwork is the world’s largest human and AI-powered work marketplace that connects businesses with independent talent from across the globe. We serve everyone from one-person startups to large organizations with a powerful, trust-driven platform that enables companies and talent to work together in new ways that unlock their potential.