You will get a custom Python event-driven quantitative backtesting engine

Project details

Most algorithmic traders lose money because their backtests are infected with look-ahead bias and completely unrealistic execution assumptions, they rely on retail platforms like TradingView that simply cannot simulate true market microstructure or handle complex multi-asset portfolio rebalancing.

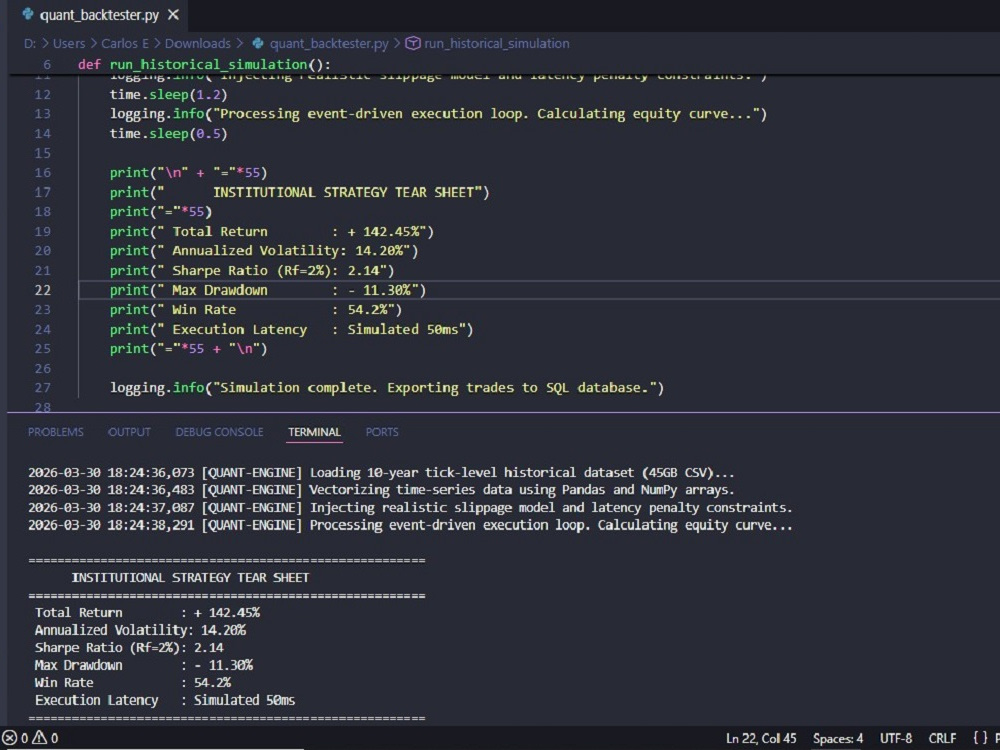

I engineer custom event-driven backtesting architectures in Python using Pandas and NumPy to process massive historical datasets. We do not just plot basic moving averages on a chart, i simulate exact slippage models, network latency delays, and institutional commission structures to give you the brutal mathematical truth about your strategy. If your algorithmic edge survives my testing environment, it actually has a statistical chance of surviving the live market, you are paying for a rigorous infrastructure that evaluates Walk-Forward Optimization and computes accurate Sharpe ratios without the illusions of retail software.

I engineer custom event-driven backtesting architectures in Python using Pandas and NumPy to process massive historical datasets. We do not just plot basic moving averages on a chart, i simulate exact slippage models, network latency delays, and institutional commission structures to give you the brutal mathematical truth about your strategy. If your algorithmic edge survives my testing environment, it actually has a statistical chance of surviving the live market, you are paying for a rigorous infrastructure that evaluates Walk-Forward Optimization and computes accurate Sharpe ratios without the illusions of retail software.

Programming Languages

Python, C#, GoCoding Expertise

Performance Optimization, SecurityWhat's included

| Service Tiers |

Starter

$550

|

Standard

$1,650

|

Advanced

$4,100

|

|---|---|---|---|

| Delivery Time | 7 days | 14 days | 25 days |

Number of Revisions | 1 | 2 | 3 |

Install Script | - | ||

Test Script | |||

Task Automation | - | - |

Frequently asked questions

About Eduardo

Senior Anti-Bot Automation Engineer & Quant Developer (Python/C++)

Divinopolis, Brazil - 8:15 pm local time

I am a Systems Engineer specialized in high-level automation and quantitative trading. I don't just write scripts. I build resilient, stealthy, and industrial-grade architectures. When it comes to anti-bot bypass and enterprise web extraction, I engineer custom headless browser stealth using Playwright, Puppeteer, and Selenium. I routinely reverse-engineer WebGL, Canvas, and WebRTC fingerprints. To bypass strict Datadome, PerimeterX, or Akamai checks, I deploy kernel-level hardware injection like virtual V4L2loopback devices. This allows complex DOM parsing and CAPTCHA circumvention for massive B2B data pipelines.

On the financial engineering side, I develop fail-safe Expert Advisors using C++ for MT4 and MT5. My algorithmic trading architectures rely heavily on Smart Money Concepts. I map liquidity sweeps, order blocks, and multi-timeframe price action entirely without lagging indicators. I also implement stealth trade management to hide stop losses and take profits from brokers, preventing virtual stop-outs. This includes real-time WebSockets integration and OS-level memory reading for dynamic web brokers. I only take on complex, high-value challenges. If your current bot is getting blocked or if you need a bulletproof financial engine ready to protect real capital, let's discuss your target and scale.

"At 6, I disassembled toys to understand their mechanics, by 12, I was captivated by the intersection of art and mathematics. I see the micro and macro connections like a musical arrangement, to me, everything is a grand opera; a harmony that makes my eyes shine."

Steps for completing your project

After purchasing the project, send requirements so Eduardo can start the project.

Delivery time starts when Eduardo receives requirements from you.

Eduardo works on your project following the steps below.

Revisions may occur after the delivery date.

Data Ingestion and Cleansing

Raw historical data is always flawed. I build the ingestion scripts to load your CSV or SQL data, scrub out anomalous price spikes, and align the time-series timestamps perfectly to prevent any look-ahead bias.

Event-Driven Engine Engineering

I code the core Python loop that steps through the historical data exactly as it would happen in real life. This forces the strategy to make decisions purely on past data while accounting for realistic trade execution delays.