You will get a clear verdict: is your trading backtest a real edge or overfit noise

Project details

You will get a clear, statistics-backed verdict on whether your trading strategy's edge is real — or just curve-fit noise that fails live.

Most backtests look great and then lose money. Two silent killers: overfitting (you tried 200 parameter combos, kept the best, and forgot you tried 200) and out-of-sample decay (the edge dies once it leaves the data it was fit on). I test for both.

Send me your strategy's realized trade returns or equity curve — no code, no API keys, no account access. I run the same three-part battery I use on my own live, capital-at-risk trading agent:

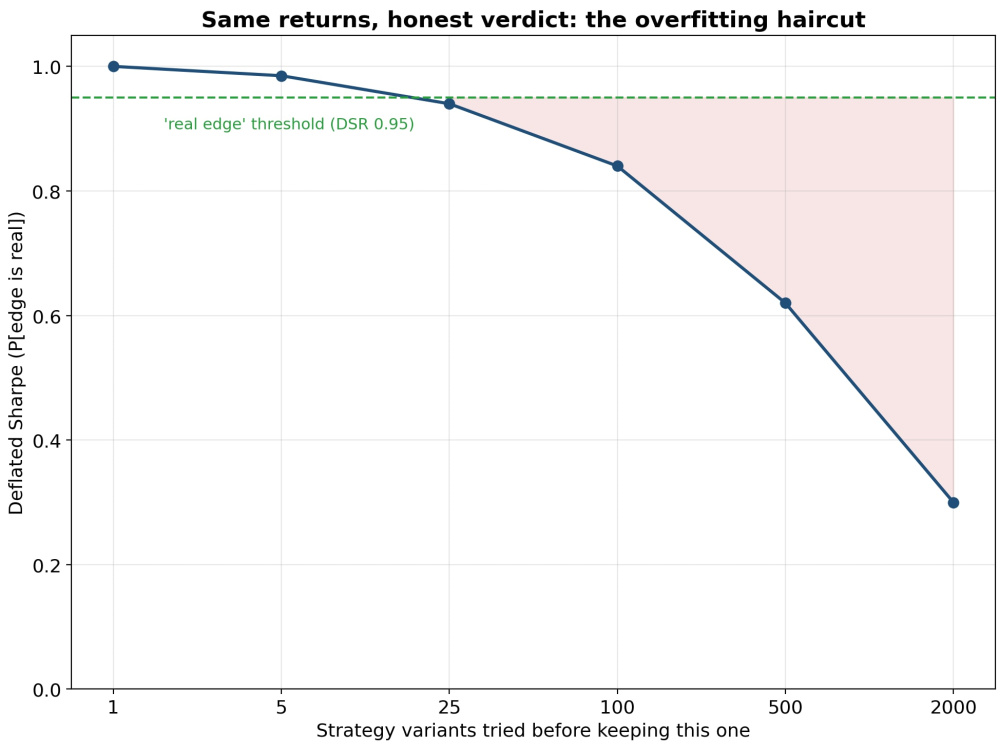

• Deflated Sharpe Ratio — haircuts your Sharpe for how many variants you tried

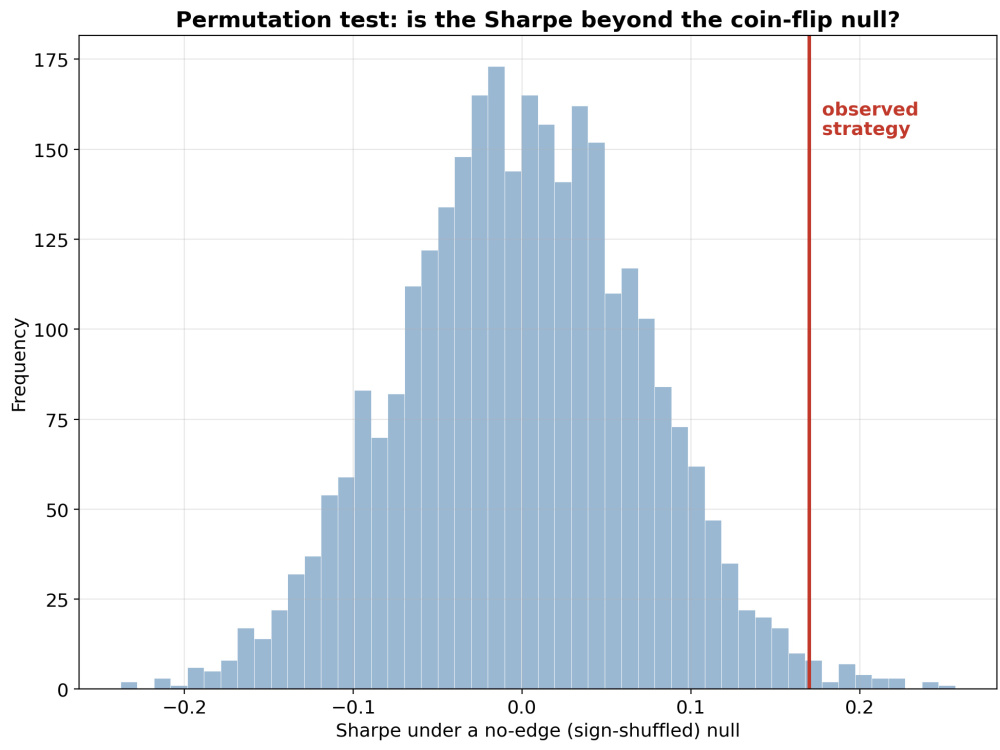

• Permutation test — how often a coin-flip reproduces your result (your real p-value)

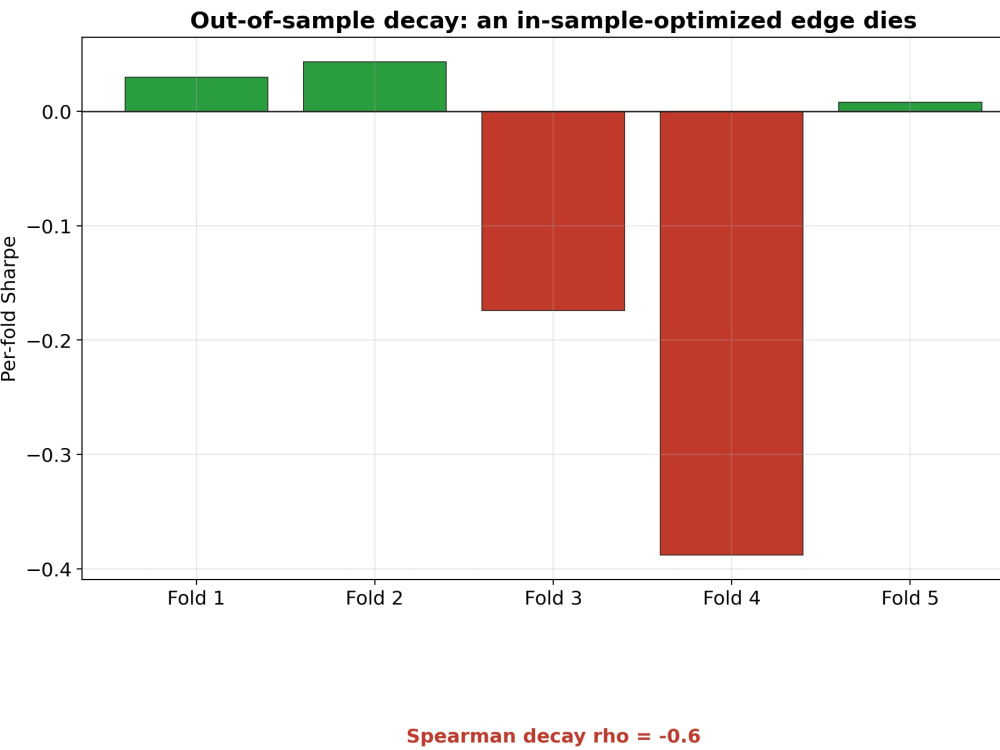

• Purged k-fold cross-validation — does the edge survive out of sample?

You get a plain-English verdict — real edge / borderline / overfit — plus the numbers behind it, so you know whether to risk capital before you do.

Background: J.P. Morgan FX & rates derivatives; I build and run production trading and evaluation systems. I'll tell you the truth — including "this one isn't real," the answer that saves you the most money.

Most backtests look great and then lose money. Two silent killers: overfitting (you tried 200 parameter combos, kept the best, and forgot you tried 200) and out-of-sample decay (the edge dies once it leaves the data it was fit on). I test for both.

Send me your strategy's realized trade returns or equity curve — no code, no API keys, no account access. I run the same three-part battery I use on my own live, capital-at-risk trading agent:

• Deflated Sharpe Ratio — haircuts your Sharpe for how many variants you tried

• Permutation test — how often a coin-flip reproduces your result (your real p-value)

• Purged k-fold cross-validation — does the edge survive out of sample?

You get a plain-English verdict — real edge / borderline / overfit — plus the numbers behind it, so you know whether to risk capital before you do.

Background: J.P. Morgan FX & rates derivatives; I build and run production trading and evaluation systems. I'll tell you the truth — including "this one isn't real," the answer that saves you the most money.

Data Tool

PythonWhat's included

| Service Tiers |

Starter

$75

|

Standard

$200

|

Advanced

$450

|

|---|---|---|---|

| Delivery Time | 2 days | 3 days | 4 days |

Number of Revisions | 1 | 2 | 3 |

Number of Graphs/Charts | 1 | 3 | 5 |

Number of Scenarios | 1 | 2 | 3 |

Number of Model Variations | 1 | 3 | 5 |

Model Documentation | - | ||

Data Source Connectivity | - | - | |

Model Validation/Testing |

Optional add-ons

You can add these on the next page.

Fast Delivery

+$40 - $150Frequently asked questions

About Federico Blanco

AI Eval Infrastructure Engineer & Agentic Systems Developer

Lewisburg, United States - 8:49 am local time

Steps for completing your project

After purchasing the project, send requirements so Federico Blanco can start the project.

Delivery time starts when Federico Blanco receives requirements from you.

Federico Blanco works on your project following the steps below.

Revisions may occur after the delivery date.

Share your data

You send your strategy's trade returns/equity as a CSV + how many variants you tried.

Validation run

I run Deflated Sharpe, a permutation test, and purged k-fold cross-validation on your returns.