You will get Development and Validation of a Probability of Default (PD) Model

Project details

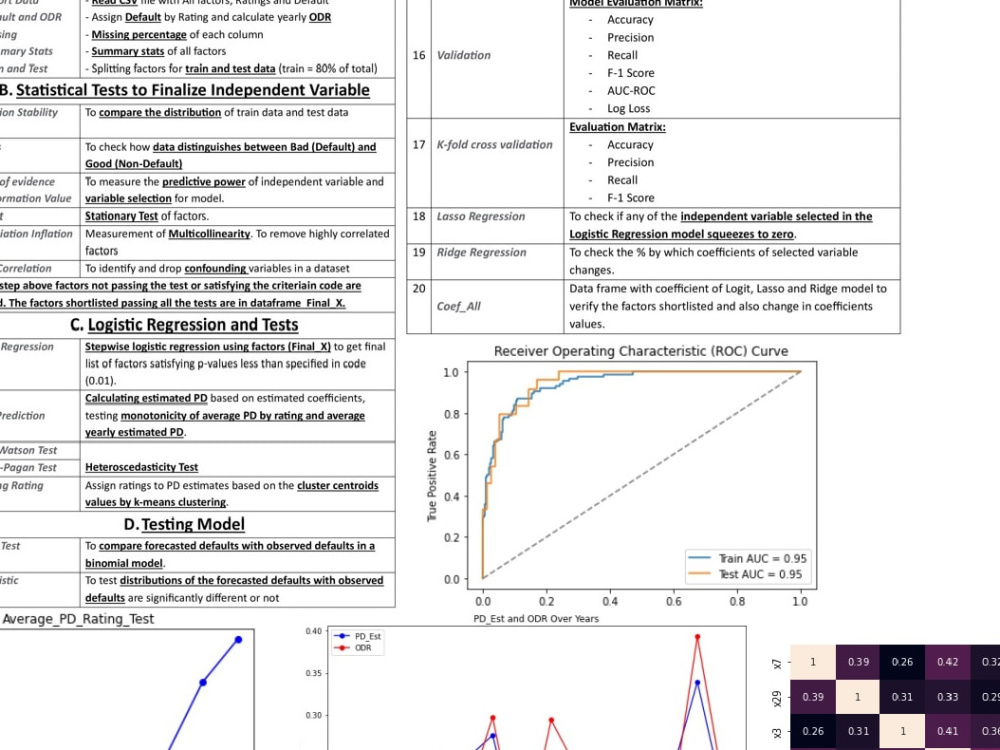

Expert PD modeling with full regulatory validation suite: 19+ statistical tests (PSI, KS, IV, adfuller, VIF, Breusch-Pagan). Comprehensive Basel-compliant validation including Jeffrey's test, ROC analysis, and k-fold cross-validation. Production-ready Python code.

Machine Learning Tools

NumPy, pandas, Python, scikit-learn, SciPyWhat's included

| Service Tiers |

Starter

$1,200

|

Standard

$1,800

|

Advanced

$3,000

|

|---|---|---|---|

| Delivery Time | 10 days | 12 days | 20 days |

Number of Revisions | 0 | 2 | 4 |

Number of Model Variations | 1 | 2 | 3 |

Number of Scenarios | 1 | 2 | 3 |

Number of Graphs/Charts | 2 | 4 | 5 |

Model Validation/Testing | |||

Model Documentation | - | - | |

Data Source Connectivity | |||

Source Code |

Optional add-ons

You can add these on the next page.

Fast Delivery

+$200 - $600

Additional Revision

+$300

Additional Model Variation

(+ 3 Days)

+$300

Additional Scenario

(+ 3 Days)

+$150

Additional Graph/Chart

(+ 1 Day)

+$100

Model Documentation

(+ 4 Days)

+$500About Nitin

Credit Risk Modeling Expert and Quantitative Research | 15+ years

Solan, India - 3:33 pm local time

I help banks, fintechs, and consultancies build regulator-ready, transparent, and robust models by applying quantitative research, econometrics, and advanced analytics.

🔹 Core Expertise

Credit Risk Modeling & Validation: PD, LGD, EAD, Stress Testing

Quantitative Research & Econometrics: Nowcasting, Yield Curve, Macro Forecasting

Regulatory Frameworks: IFRS9, Basel IRB, CECL, CCAR

Advanced Analytics: Scenario Analysis, Sensitivity Testing, Survival Analysis

Automation & Data Analytics: Python, SAS, R

🔹 Why Clients Work With Me

Proven track record with EY, ING, Barclays, HSBC, Citi, and HDFC

Blend of quantitative research + regulatory knowledge, ensuring compliance & innovation

Skilled communicator with C-Suite & regulator engagement experience

Known for integrity, professionalism, and delivering results

Goal: Help financial institutions manage risk smarter, stay compliant, and unlock actionable insights through advanced analytics and quantitative research.

Steps for completing your project

After purchasing the project, send requirements so Nitin can start the project.

Delivery time starts when Nitin receives requirements from you.

Nitin works on your project following the steps below.

Revisions may occur after the delivery date.

Data Validation & Preprocessing

Verify data structure and quality checks Handle missing values and outliers Create default flags

Feature Selection & Analysis

Perform PSI stability testing Conduct KS-statistic analysis Calculate WOE/IV for predictive power